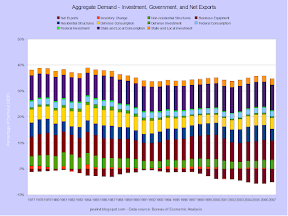

Apropos of the post prior to the previous post, here are some very simple revenue projections for taxes other than the personal income tax.

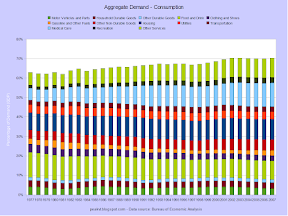

Since it is assessed at a flat rate, a value-added tax is regressive. Poorer people, who spend a greater amount of their income, end up paying more tax as a percentage of their income than the well-off do with a VAT, or with any other consumption tax for that matter. This can be somewhat mitigated by excluding certain items. Food and housing are the most common. If consumption stays at 70% of GDP, a 12% VAT excluding food and housing would yield just about 6% of GDP. If consumption falls to 58% the rate would have to go to 15%. For comparison, the median rate in the EU is 20%.

Since it is assessed at a flat rate, a value-added tax is regressive. Poorer people, who spend a greater amount of their income, end up paying more tax as a percentage of their income than the well-off do with a VAT, or with any other consumption tax for that matter. This can be somewhat mitigated by excluding certain items. Food and housing are the most common. If consumption stays at 70% of GDP, a 12% VAT excluding food and housing would yield just about 6% of GDP. If consumption falls to 58% the rate would have to go to 15%. For comparison, the median rate in the EU is 20%.

Ah, the gas tax. One would think after two wars directly related to oil (yep, they were) people would be gung-ho about this source of revenue. The current federal gas tax is $0.184 per gallon, with an additional $0.00 (Alaska) to $0.416 (New York) in state taxes. Taxes on diesel are slightly higher. Increasing the federal tax to $1.50 would yield about 1.5% of GDP at the current consumption rate of 9.5M barrels per day. The total pump price would go up to about $4.00 per gallon.

Ah, the gas tax. One would think after two wars directly related to oil (yep, they were) people would be gung-ho about this source of revenue. The current federal gas tax is $0.184 per gallon, with an additional $0.00 (Alaska) to $0.416 (New York) in state taxes. Taxes on diesel are slightly higher. Increasing the federal tax to $1.50 would yield about 1.5% of GDP at the current consumption rate of 9.5M barrels per day. The total pump price would go up to about $4.00 per gallon.

This is an attempt to look at a carbon tax in a slightly more sophisticated way - but I don't have a background in economics so this initial cut could be completely wrong. Anyway, there are three sets of lines - no reduction, a 2% decrease for each $5 per ton increase in the tax, and a 4% decrease. Applying the 2% factor resulted in consumption falling by 45% at the highest price, and the 4% factor resulted in a reduction of 70%. Nice results, but they in no-way reflect what might happen if a big tax was slapped on tomorrow - pure chaos. But applied over time - increasing by $5 per year, and by $10 after several years - there would be significant reductions without harm to the economy, though the change in consumption would not follow a simple curve.

This is an attempt to look at a carbon tax in a slightly more sophisticated way - but I don't have a background in economics so this initial cut could be completely wrong. Anyway, there are three sets of lines - no reduction, a 2% decrease for each $5 per ton increase in the tax, and a 4% decrease. Applying the 2% factor resulted in consumption falling by 45% at the highest price, and the 4% factor resulted in a reduction of 70%. Nice results, but they in no-way reflect what might happen if a big tax was slapped on tomorrow - pure chaos. But applied over time - increasing by $5 per year, and by $10 after several years - there would be significant reductions without harm to the economy, though the change in consumption would not follow a simple curve.

For reference, the Iraq War has cost about $600B so far, and the total long term cost will be much higher. If we had tried to pay for the war in real-time, a gas tax of $1.00 or $1.25 would have covered it.