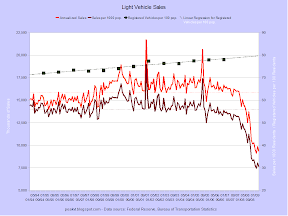

One final graphy post for today. The set contains some slightly encouraging news about debt, but very discouraging news about assets.

Assets are evaporating but debt isn't, as expected.

Assets are evaporating but debt isn't, as expected.

We can safely say we've never seen wealth destruction like this before.

We can safely say we've never seen wealth destruction like this before.

Real estate is actually increasing its share of Americans' net worth.

Real estate is actually increasing its share of Americans' net worth.

That is because financial assets are more volatile than real estate.

That is because financial assets are more volatile than real estate.

I forget what "other" liabilities are, and I'm too tired to look it up right now.

I forget what "other" liabilities are, and I'm too tired to look it up right now.

In nominal terms mortgage debt has stopped increasing. That means it is falling in real terms, albeit slowly because inflation is near zero.

In nominal terms mortgage debt has stopped increasing. That means it is falling in real terms, albeit slowly because inflation is near zero.